The insurance for outstanding medical care and financial security

SWICA also supports you in your efforts to stay healthy and rewards you for activities relating to exercise, nutrition and relaxation. Thanks to BENEVITA you can benefit from your healthy lifestyle. Sign up for this free bonus programme and receive additional discounts on the premiums for a range of supplementary insurance plans.

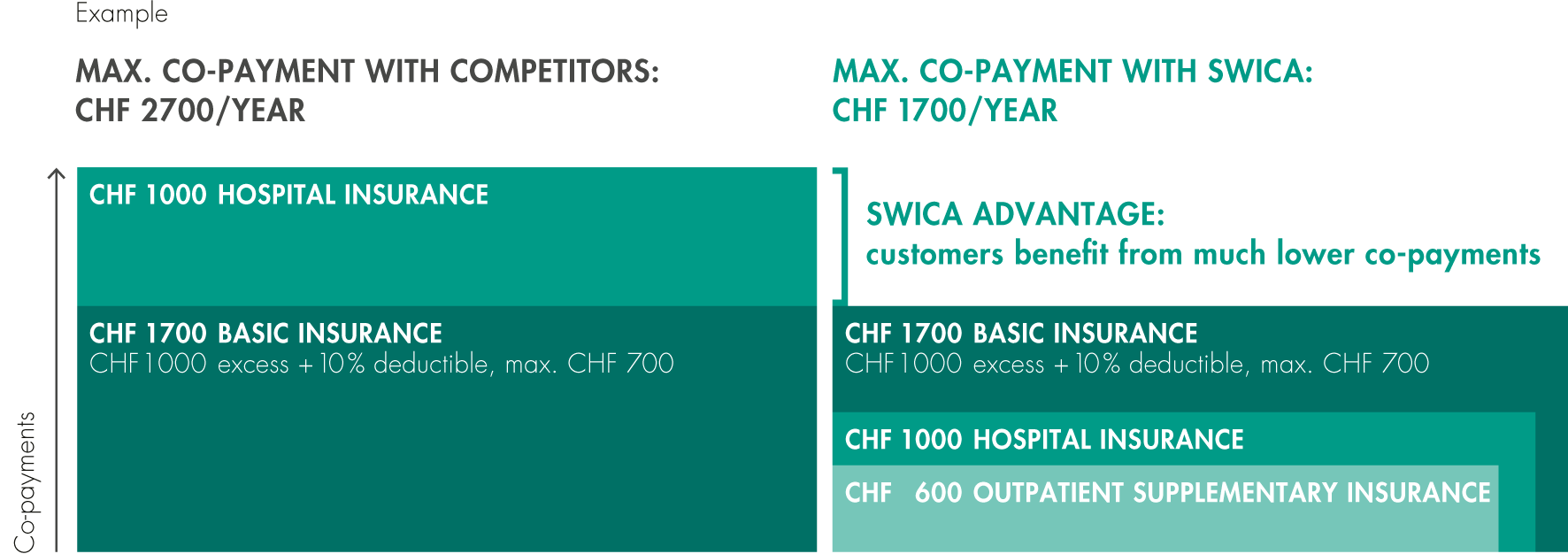

Your SWICA advantages

SWICA's partnerships with many businesses and associations enable their employees and members to enjoy group discounts on supplementary insurance plans, annual sports contributions and other preferential offers.

As SWICA does not have multi-year contracts, customers can benefit from maximum freedom of choice and always get the right kind of cover.

Learn more

More

SWICA supports over 100 offers and courses for health promotion and preventive healthcare. In the areas of exercise, nutrition, relaxation and wellbeing (e.g. fitness, sports associations, dance classes, nutritional advice, mindfulness training, swimming pools and saunas) SWICA rewards your healthy and preventive lifestyle by making attractive contributions of up to 1'300 francs (learn more) per year.

+41 44 404 86 86.

Professional care management: In the event of illness or accident you can count on professional support from experienced SWICA care managers who will advise and support you in choosing the right treatment and help you out on the administrative front. SWICA has more than 85 care managers working for customers across Switzerland.

Home Nanny and Home Attendant services: SWICA can ensure that your child and household are cared for while you are in hospital or at a medical spa. SWICA customers receive professional support through the Home Nanny and Home Attendant services.

SWICA believes that conventional medicine and complementary medicine can be combined to good effect. Anything that benefits your health is a good thing. That’s why SWICA supports complementary therapy methods and puts them on an equal footing.

Complementary treatment methods include acupuncture, aromatherapy, the Feldenkrais method, fango mud therapy, cupping, Rolfing, Bach flower remedies, ayurvedic medicine, biodynamics, spagyrics, Kneipp therapy, shiatsu massage, qigong and much more.

SWICA helps you to adopt a healthy lifestyle and reward you for doing so. Collect points with the BENEVITA app, learn about health topics, enjoy attractive offers, and benefit from discounts of up to 15% (learn more) on the COMPLETA TOP, COMPLETA FORTE and HOSPITA supplementary insurance plans.

You can contact our customer service desk on 0800 80 90 83 or +41 52 244 28 28 – 24 hours a day, 7 days a week.

The health insurance system in Switzerland

- Who is obliged to have basic insurance cover?

- When does health insurance have to be purchased?

- Which benefits are provided under basic insurance cover?

- Do I have to contribute towards my healthcare costs?

- How do I choose the right excess?

- If the benefits provided by all insurers are the same, why do the premiums for basic insurance vary so much?

- Who pays the health insurance premiums?

- What happens if you miss the three-month deadline for registering with an insurance company?

- Does the basic insurance cover treatment costs in my home country?

- How are the costs reimbursed to the insured person by the insurance company?

- Where can I find more detailed information about the benefits that are covered by the mandatory basic insurance?

- How can I reclaim from the insurer the money that I myself have paid for treatment?

- What insurance cover do I have under the law in Switzerland?

Who is obliged to have basic insurance cover?

Under the Federal Health Insurance Act (KVG), every person resident in Switzerland must have at least mandatory basic insurance.

Families must take out separate basic insurance for each member of the family, regardless of age.

When does health insurance have to be purchased?

You have three months from the date on which you register with the residents' registration office to register with a health insurer for mandatory basic insurance. Because insurance cover begins as soon as you register with the residents' registration office, the premiums for basic insurance are owed with effect from the month of registration. This means that you may have to make more than one month’s payment when you pay for the first time.

Which benefits are provided under basic insurance cover?

The medical benefits covered are regulated by law and are the same with all insurance providers. Insurance companies are obliged to accept all applications for basic insurance.

Do I have to contribute towards my healthcare costs?

Yes, it is obligatory in Switzerland to contribute towards your own healthcare costs. This contribution is levied through the annual excess and the deductible. The excess is the annual amount which the insured person must contribute towards the services which he/she uses. Individuals can select the level of excess that suits them. The options for excesses are defined in law and are set at CHF 300 to CHF 2,500 for adults. Once the excess has been paid, the insured person is also responsible for paying the deductible, which is 10% of the relevant healthcare costs. However, the deductible never exceeds 700 francs per calendar year. So, with an excess of CHF 300, the maximum cost to the insured person would be CHF 1,000.The excess and deductible are lower for children. The larger the excess, the lower the monthly premium.

How do I choose the right excess?

The right choice of excess depends on the expected healthcare costs. The larger the excess you choose, the lower your monthly premium will be. Therefore, if you expect your monthly healthcare costs to be low, you would usually choose a large excess and so keep your insurance costs to a minimum. The options for excesses are defined in law and are set at CHF 300 to CHF 2,500 for adults.

If the benefits provided by all insurers are the same, why do the premiums for basic insurance vary so much?

The basic insurance provides all insured persons with the same scope of cover. The premium to be paid depends on the insured person’s place of residence and age. However, insurance costs can be significantly reduced depending on the basic insurance model chosen.

Who pays the health insurance premiums?

In Switzerland, unlike in other countries, premiums are paid in full by the insured person. Depending on the insurance company, the insured person can choose the payment frequency.

What happens if you miss the three-month deadline for registering with an insurance company?

If you miss the registration deadline, you will be assigned to a statutory health insurer by your municipality and a premium surcharge will apply.

Does the basic insurance cover treatment costs in my home country?

You can only have medical treatment in Switzerland, even if the costs are lower in your home country.

How are the costs reimbursed to the insured person by the insurance company?

Normally the doctor's bill is sent directly to the health insurer from the doctor’s practice. To take advantage of this facility you must present your insurance card when you register with a doctor. The practice may, however, send the invoice directly to you. In this case you would pay the bill and submit the paid invoice to the health insurer. If you are entitled to reimbursement, the amount in question will be transferred to you by the health insurer.

Where can I find more detailed information about the benefits that are covered by the mandatory basic insurance?

Every health insurer will be happy to provide you with more detailed information about the benefits available under the mandatory basic insurance. Make an appointment with the health insurer of your choosing.

How can I reclaim from the insurer the money that I myself have paid for treatment?

As a rule, invoices which you have settled yourself can be submitted to the health insurer either digitally or by post. Submitted invoices are checked and, if you are entitled to reimbursement, the sum in question will be transferred to you. This process generally takes a few days.

What insurance cover do I have under the law in Switzerland?

In Switzerland there are a number of statutory social insurance providers and schemes. You'll find an overview in our fact sheet on social insurers in Switzerland.

- Do I have to take out supplementary insurance?

- Which benefits does supplementary insurance provide?

- When can I purchase supplementary insurance?

- How can I take out supplementary insurance?

- Can a health insurer turn down my application for supplementary insurance?

Do I have to take out supplementary insurance?

No, supplementary insurance is voluntary. It is used to top up the benefits available under the mandatory basic insurance in line with the insured person's individual needs.

Which benefits does supplementary insurance provide?

Supplementary insurance tops up the benefits available under the mandatory basic insurance in line with the insured person's individual needs. For example, supplementary insurance could cover benefits in the field of complementary medicine, the cost of glasses and contact lenses, dental treatment and much more. Personal advice from an expert will help you to find the supplementary insurance plan that is right for you.

When can I purchase supplementary insurance?

Supplementary insurance can be purchased at any time.

How can I take out supplementary insurance?

An insurance advisor is the right person to approach for advice in this area. He will put together a personal quotation that is tailored to your needs. You will have to complete a medical check before you can buy supplementary insurance. This will also be provided by the insurance advisor. The insurance application is then submitted and checked by the health insurer. Usually you will be informed in writing if your application is successful. Health insurers are entitled to accept an application in full, accept it with certain exclusions, or reject it.

Can a health insurer turn down my application for supplementary insurance?

Yes, health insurers can reject an application in part (i.e. by specifying exclusions) or in full if the applicant has previously suffered a serious illness or accident. However, it is always possible to take out basic insurance.

- Do I have to take out hospitalisation insurance?

- In which hospitals will I be treated if I don’t have hospitalisation insurance?

- What level of costs can I expect if I receive inpatient treatment?

Do I have to take out hospitalisation insurance?

No, under the Federal Health Insurance Act only the basic insurance is mandatory for people living in Switzerland.

In which hospitals will I be treated if I don’t have hospitalisation insurance?

As a matter of principle you can be admitted to any hospital in Switzerland. However, if you do not have hospitalisation insurance, the costs are only covered up to the amount that would be covered for the same treatment in your canton of residence. Since treatment costs vary from canton to canton, insured persons may face additional costs as a result. The only exception is if the treatment required is unavailable in your canton of residence.

What level of costs can I expect if I receive inpatient treatment?

When you buy hospitalisation insurance, you select a deductible of between CHF 0 and CHF 5,000, representing your contribution towards the cost of hospital treatment.

SWICA is the only health insurer that applies co-payments from basic insurance to those of its supplementary insurance, which means the annual co-payments will be much lower when compared to other health insurers.